Power Plant (Tianjin, China) by Shubert Ciencia on Flickr.

Too Big to Unwind? About the Current State of China’s Coal Sector

Beneath the headlines about China's renewable-energy boom, coal remains deeply embedded in the country's economy. This article explores why China's dependence on coal persists and how the industry's "greening" masks the true scale of that reliance.

By Belinda Uebler

Quick Takes

- Despite rapid renewable expansion, China continues to build new coal-fired power plants and increase coal output, underscoring the coal sector’s deep economic and political role in China’s development model.

- China still lacks a clear coal phase-out strategy. Decarbonization remains fragmented, while coal-dependent cities are experimenting with industrial diversification and tourism as alternative growth models.

- Coal-dependent regions face deep structural constraints: slower growth, population decline, and limited investment, reinforcing reliance on coal in many regions.

- Coal-based industries remain central to China’s economy, including coal-to-chemicals, and coal-based hydrogen. Framed as green transition strategies, they often amount to rebranded continuity rather than true transformation.

As countries around the world struggle to honor their climate pledges, China appears to have found an effective way to improve its emissions record: changing how it counts. According to a recent report by the Centre for Research on Energy and Clean Air (CREA), Beijing has revised its carbon-accounting methodology, altering the calculation of carbon intensity in a way that excludes certain non-energy uses of fossil fuels. As a result, China's reported emissions growth between 2020 and 2025 was effectively halved on paper, creating a statistical gap of roughly 730 million tonnes of CO₂ annually. The revision lowers the threshold for meeting China's climate targets, allowing the country to appear closer to fulfilling its 2030 commitments even if its absolute emissions continue to rise.

This episode is just one example of the broader challenge of understanding China's carbon footprint. In recent years, optimistic headlines about falling CO₂ emissions and efforts to curb coal-fired power generation have fostered the impression that the country is on a clear and rapid path toward decarbonization. Yet such narratives often obscure the structural realities of China's energy system and its long-term trajectory. Behind the stories celebrating record growth in renewable capacity lies a more complicated coal story. Although China’s renewable buildout is substantial, it coexists with a large, hard-to-abate coal sector that remains deeply embedded in industrial production and the overall energy mix, underscoring the continued expansion and central role of coal in electricity generation.

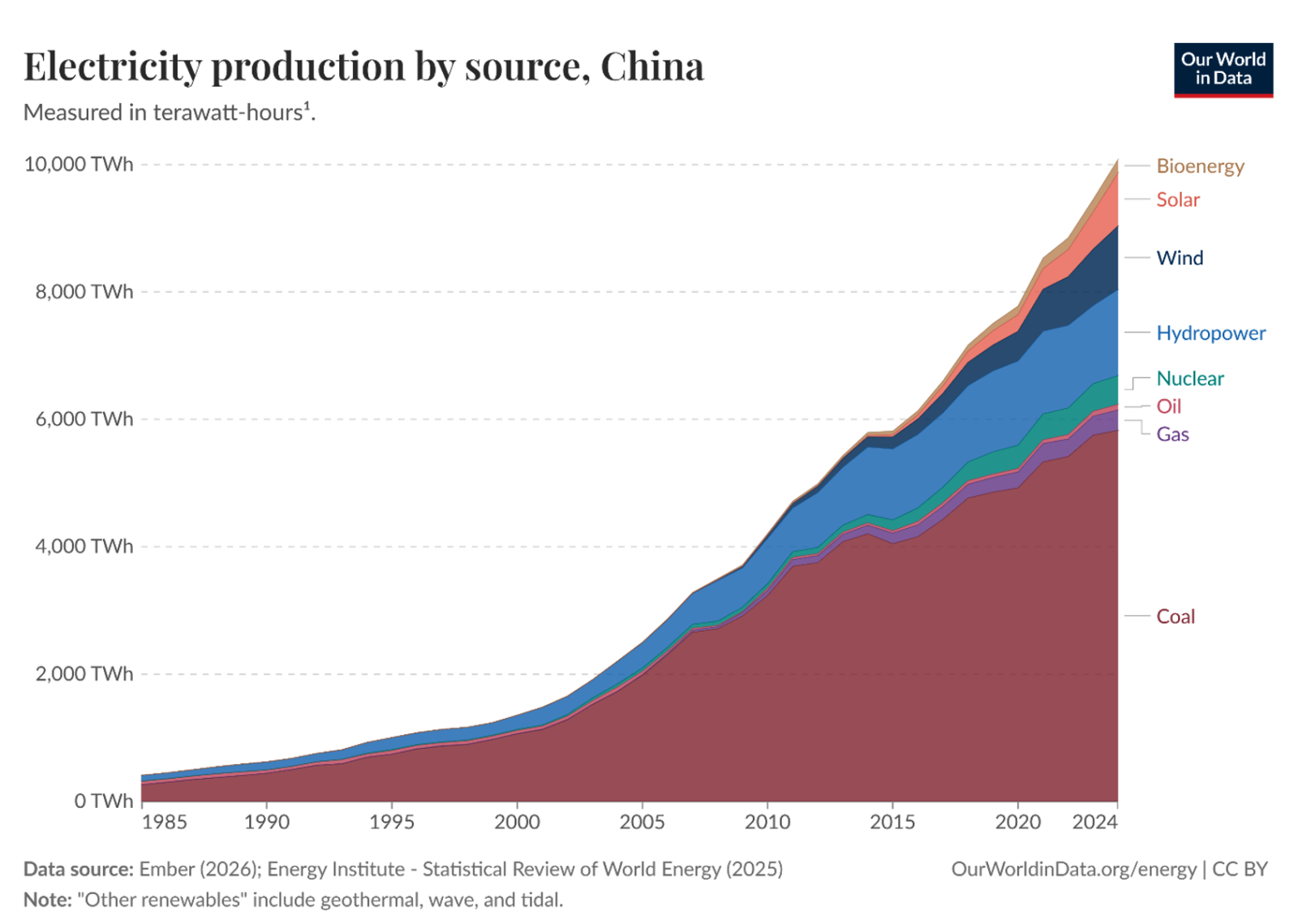

In recent years, China’s rapid expansion of renewable energy capacity has had profound effects on its traditionally coal-dominated energy system. In 2024 and 2025 alone, China installed 360 and 430 gigawatts of wind and solar capacity, respectively. In 2024, this represented roughly 64% of all new solar and wind installations worldwide. Most notably, as of February 2025, for the first time, wind and solar energy together – reaching a total installed capacity of 1.45 billion kW – have overtaken coal power, becoming China’s largest electricity source in terms of installed capacity.

This, however, does not mean that renewable energy has already displaced thermal power such as coal, despite increases in installed capacity. Chinese data, and increasingly global data, tend to report installed capacity, which indicates the potential maximum output, rather than operational or actually producing capacity. In practice, especially in China, only a fraction of installed renewable capacity is actively generating electricity at any given time due to storage limitations and grid dispatch constraints, among other factors. Consequently, when examining China’s energy mix, which reflects the energy actually consumed by society, coal energy still accounts for the majority, representing 55.5 percent of the total between October 2024 and September 2025. Moreover, as China’s total energy demand continues to rise, the absolute amount of coal-fired electricity generation increased for many years and only declined for the first time in 2025, by 1.6% year on year.

Our World in Data. 2025. “Electricity Production by Source, China.”

Against the backdrop of global climate targets and China’s commitments to peak carbon emissions by 2030 and achieve carbon neutrality by 2060, deep decarbonization has become an essential policy objective. Achieving these goals requires a comprehensive energy transition, as the energy sector constitutes a central source of CO₂ emissions. A key component of this transition is the gradual phase-out of coal. In China, however, the coal sector is deeply embedded in the country’s economic structures, regional development, and energy system, making a rapid exit particularly challenging. Against this background, this paper examines the current state of China’s coal sector and analyzes the economic, structural, and political challenges associated with a necessary phase-out of coal in China.

Where China’s Coal Industry Stands Today

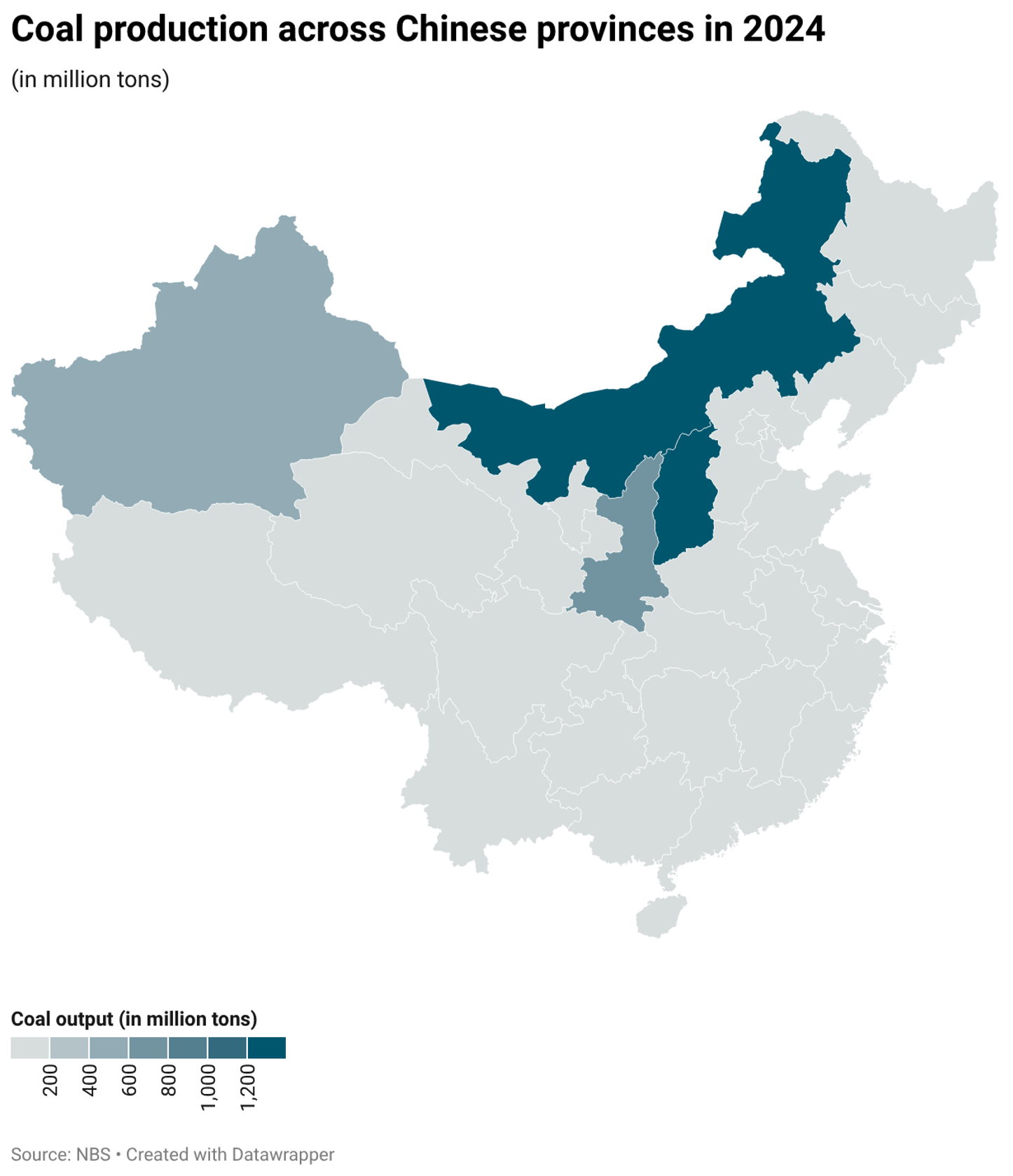

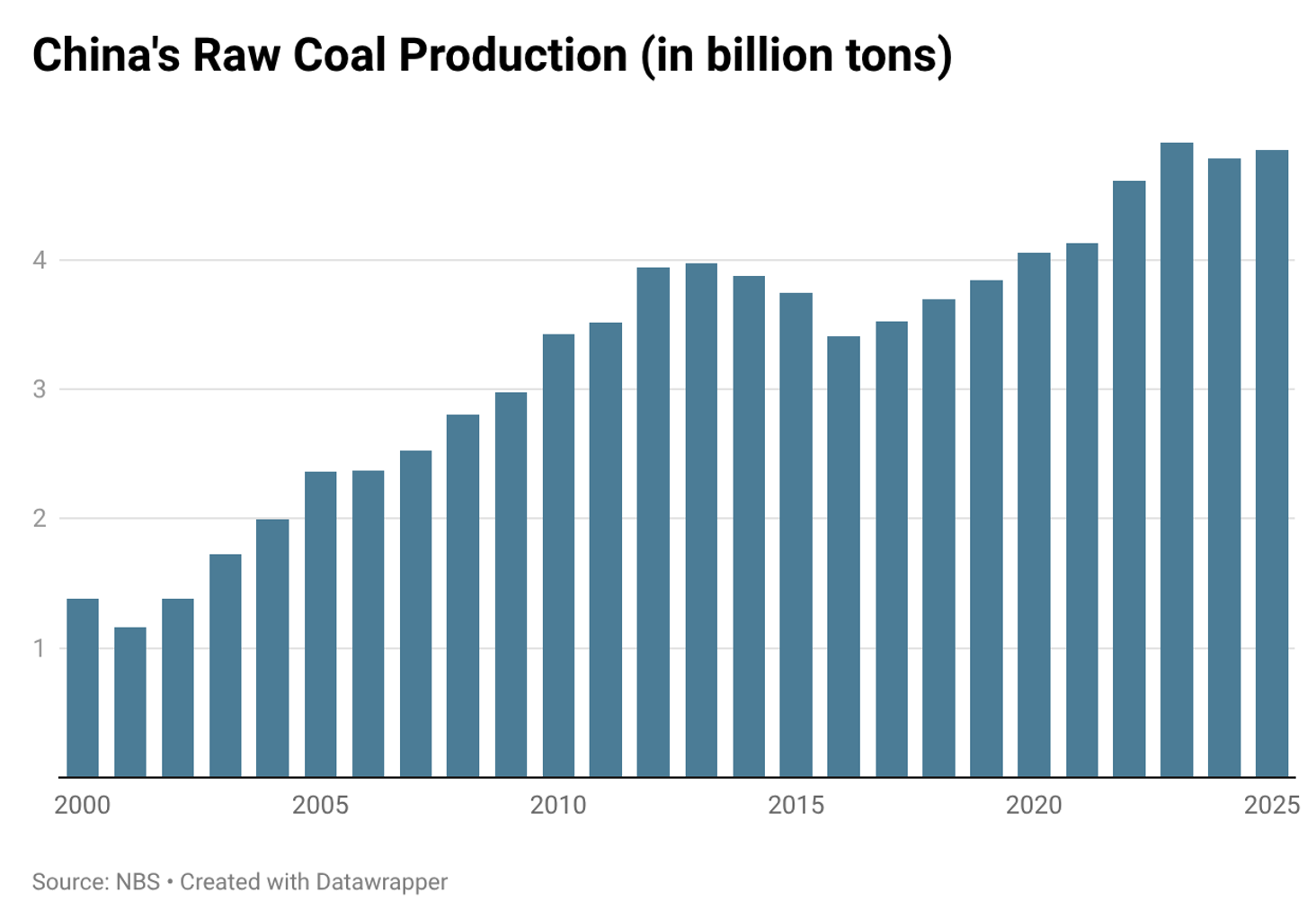

Despite China’s rapid expansion of renewable energy installations, the country has also continued building coal-fired power plants, reaching a 10-year high of 94.5 gigawatts in 2024, driven by rising energy demand and concerns over energy security. In 2025, a record number of coal power plants were newly commissioned, alongside unprecedented levels of project starts and reactivations. Coal mining output has likewise increased to record levels in recent years, following a period of stagnation and slight decline throughout much of the 2010s. This simultaneous growth in renewables and thermal energy shows that isolated figures can be misleading without considering the full context of the country’s energy transition.

Merely in terms of coal sector employment, the situation looks clearly different. Following a series of environmental regulations and policies aimed at reducing coal overcapacity in the 2010s, numerous closures and layoffs occurred within China’s coal sector. As a result, coal employment has fallen to historically low levels in recent years, declining by around 50% between 2013 and 2022 in coal mining, washing, and dressing. However, precise figures are difficult to determine, as actual employment numbers may be somewhat higher than officially recorded.

Despite declining coal employment, coal remains central to China’s energy system. The overwhelming majority of coal production is directed toward industry, where it is consumed either in its original form or as heat or electricity. Consequently, China’s industry would be most affected by a structural phase-out of coal, while other end-use sectors such as residential, commercial, agricultural, and transport account for only a marginal share and would be comparatively less affected.

Thus, despite growing narratives of a ‘greening’ China driven by the rapid expansion of renewable energy, a more accurate picture recognizes the continued existence and dominance of a large, hard-to-abate coal sector. This sector continues to fuel China’s industry and remains a central component of the energy mix, even amid rising renewable capacity installations.

Tentative attempts at transformation

Despite China’s dual carbon goals – peaking CO₂ emissions by 2030 and achieving carbon neutrality by 2060 – there is still no consistent, nationwide phase-out of coal. Instead, China has implemented a series of mostly isolated decarbonization policies and emission reduction targets that are partly intended to support the dual carbon goal, but vary in strictness across regions and political priorities. Decarbonization policies include such on the closure of coal mines and coal-fired power plants, particularly smaller facilities with poor environmental standards, as well as plant and mine shutdowns aimed at reducing air pollution among others. They also encompassed the closure of coal-based production capacities in the steel or aluminium sectors, or banning coal as a heating source in rural areas of northern China.

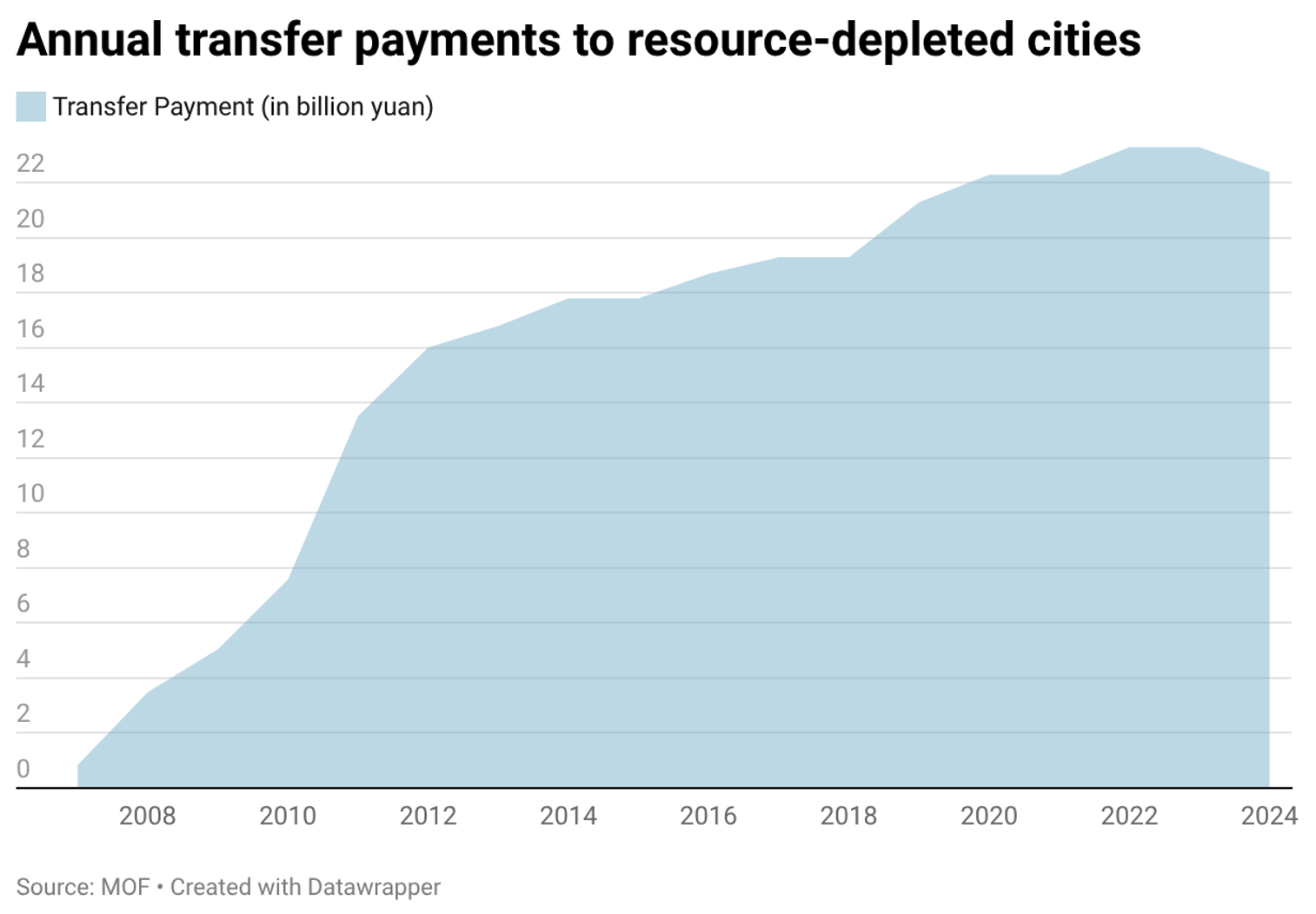

One of the most notable examples of a cross-sectoral and multidimensional policy aimed at transitioning away from coal in China so far is the transformation of coal resource-depleted cities. In the 2000s, the Chinese government began addressing the growing number of resource-depleted cities across the country, which were struggling with structural economic problems. Between 2008 and 2012, the central government officially designated 69 resource-depleted cities, including 37 coal resource-depleted cities, although the current actual number is likely much higher. These officially recognized resource-depleted cities received and still receive support from the government, particularly in the form of transfer payments to support social security, education and healthcare, environmental protection, public infrastructure construction, and interest subsidies for special loans in these cities. The transfer payments were conceived as time-limited from the outset, initially for three to four years from 2007 to 2010. Later, the possibility of extensions was announced, followed by plans for a phased withdrawal. In practice, however, new extension options continued to be introduced, and transfer payments to resource-depleted cities are still being made to this day.

Although transfer payments have increased in absolute terms in recent years, when compared to the budgets of the affected cities, these payments provide limited support, and may thus not be sufficient as a long-term strategy for facilitating the transformation. In this context, some cities have been reportedly unenthusiastic about applying for these transfer payments because the amounts are relatively small.